ACH Return Code Delay Explained: Why ACH Payments Return Late

Learn what ACH return code delay means, why ACH returns take time, and how banks process delayed ACH failures. Simple guide for businesses and payment users.

2/22/20262 min read

You sent an ACH payment. Everything looked fine. Then days later, the transaction suddenly returned with a code.

This situation confuses many people. They assume ACH failures happen instantly. In reality, ACH returns often appear after a delay. That delay is normal in the banking system.

Understanding ACH return code delays helps businesses manage cash flow, avoid accounting mistakes, and respond faster when payments fail.

Let’s break it down in simple terms.

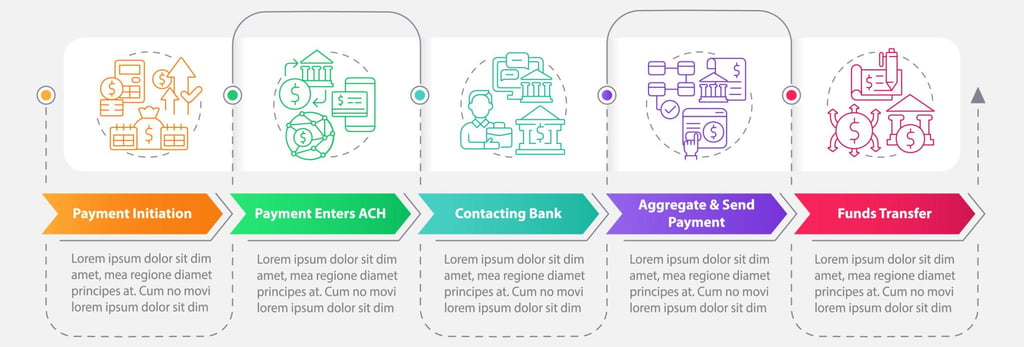

Background: How ACH Processing Actually Works

ACH transfers do not move in real time like card payments.

Instead, they move in batches through the Automated Clearing House network. Banks review transactions after receiving them. During this review period, problems can still be discovered.

That is why an ACH payment can look successful at first but still be returned later.

The delay is built into the system itself.

What “ACH Return Code Delay” Really Means

An ACH return code delay means:

The receiving bank detected a problem after initial processing and sent the payment back later.

The delay does not mean the bank is slow. It means the system allows time for verification.

This protects both banks and customers from fraud, errors, and unauthorized withdrawals.

Common Reasons ACH Returns Are Delayed

1. Insufficient Funds Discovered After Posting

Sometimes funds appear available during processing but are removed before final settlement.

Example:

A customer spends money after your ACH debit begins. The account then fails during final review.

The return may appear 1 to 2 business days later.

2. Account Status Changes

Accounts can change suddenly:

Account closed

Account frozen

Legal hold placed

Fraud investigation started

If this happens during clearing, the return comes later instead of instantly.

3. Unauthorized Transaction Claims

This is one of the biggest causes of delayed ACH returns.

Consumers can dispute ACH debits as unauthorized for up to 60 days.

When this happens, the bank sends an ACH return code like:

Unauthorized debit

Authorization revoked

Customer dispute

These returns can appear weeks after the original payment.

4. Administrative Bank Corrections

Banks sometimes need time to verify:

Incorrect account numbers

Name mismatches

Routing issues

Format errors

Once confirmed, the return is issued.

Typical ACH Return Delay Timeframes

Here is what most businesses see in practice:

1–2 business days

Standard administrative returns such as insufficient funds or invalid account.

3–5 business days

Processing issues, account closures, or bank verification delays.

Up to 60 days

Consumer unauthorized transaction disputes.

Even longer in rare corporate dispute cases

This wide timing range surprises many new ACH users.

Why ACH Delays Matter for Businesses

Delayed returns can create real problems:

Revenue appears collected but later disappears

Accounting reports show incorrect balances

Services may be delivered before payment truly clears

Subscription billing may fail unexpectedly

This is why experienced finance teams never treat ACH as fully cleared immediately.

Instead, they monitor transactions for several days.

How to Protect Yourself From ACH Return Delays

Verify bank accounts before first charge

Use account validation tools or micro-deposit verification.

Wait before delivering high-value services

For large payments, many companies wait 3 to 5 business days.

Keep written authorization records

This protects you if a customer disputes the payment weeks later.

Track return codes daily

Payment dashboards should be checked every day to catch late returns fast.

Simple Rule to Remember

ACH payments are fast, but they are not instant.

A payment appearing successful today does not guarantee it will stay successful tomorrow.

Understanding this single rule prevents most ACH cash flow surprises.

Conclusion

An ACH return code delay is not a system error. It is a normal part of how the banking network protects transactions.

Returns may happen days or even weeks later depending on the issue. Businesses that understand this timing can plan better, avoid accounting shocks, and reduce payment risk.

If you handle ACH payments regularly, building a short monitoring window into your workflow can save serious time and money.